Inflation creeps higher as supply lags demand

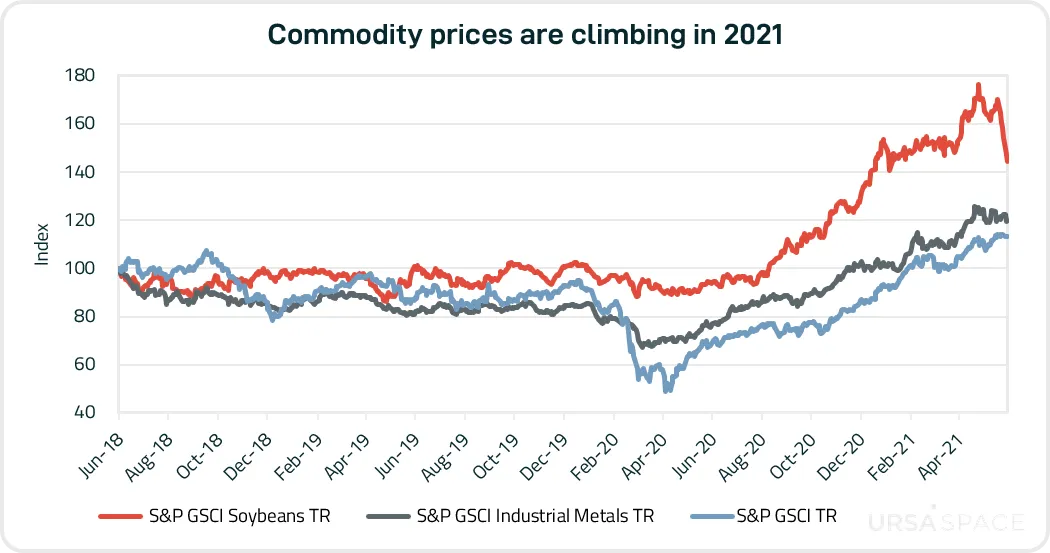

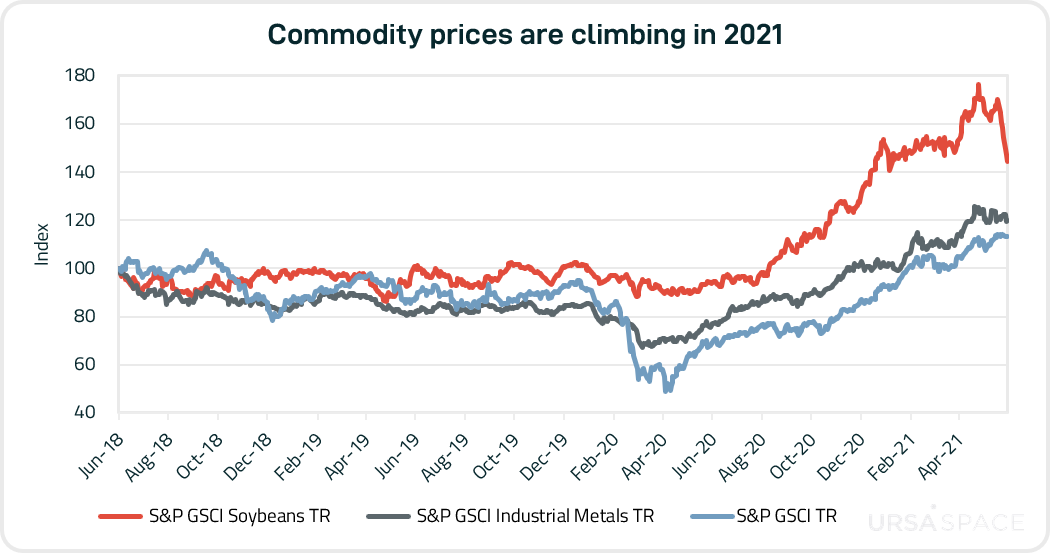

The S&P GSCI, a widely-followed barometer of commodity prices, the S&P GSCI Soybean index and the S&P GSCI Industrial Metals index.

With an eye on inflation, the Federal Reserve on June 16 moved forward the date for lifting interest rates from 2024 to as early as 2023.

In this blog, we focus on insights revealed through a pair of datasets created by Ursa Space derived from synthetic aperture radar (SAR), an all-weather, 24/7 satellite technology.

The two datasets cover crude oil inventories and auto manufacturing, both of which are considered significant sectors of the global economy and can provide macroeconomic signals.

The graphic below shows our global coverage for crude inventories, auto manufacturing and port monitoring, which we’ll discuss in future blogs (stay tuned!).

Crude Oil Inventories

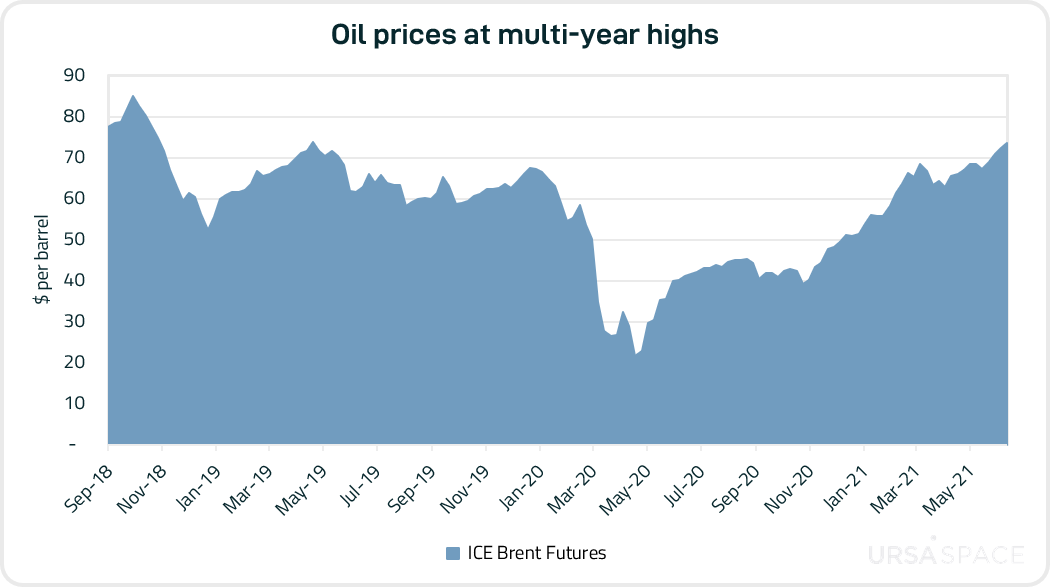

Crude oil prices have increased recently, translating into higher prices at the pump. Global benchmark ICE Brent is close to $75 per barrel, a level not seen since late 2018, and up from about $50/b at the start of 2021 and nearly doubling year-on-year.

Do fundamentals support higher prices?

The best indicator of the global supply-demand balance is the amount of oil in storage. Ursa Space measures approximately 20,000 storage tanks every week, totaling more than 6.6 billion barrels of total capacity in 123 countries.

Ursa Space data shows global crude oil inventories peaked in October 2020. Since then, they have dropped below 2020 levels, and even returned to 2019 levels for the same time of year, which are a better indication of “normal” conditions.

The message that “oil inventories are returning to pre-pandemic norms” was delivered this week to an audience attending the S&P Global Platts Global Executive Petroleum Virtual Conference, during a featured panel discussion on oil storage markets that included Daniel Baruch, Ursa Space’s Director of Global Energy Markets & Business Development.

Other takeaways from Daniel included:

- Global crude oil inventories stand about 5% below the October 2020 peak

- China was the main driver behind higher inventories in 2020 and the declines over the last eight months

- A big wildcard in 2021 will be exports from Venezuela and Iran, both of which face US sanctions aimed at curbing the sale of oil abroad

- Venezuelan crude oil inventories at the country’s main export terminal (El Jose) are roughly one-half of the level observed last year at this time, on account of a pick-up in exports, mostly headed to China

- Iran’s crude inventories, usually quite volatile, have marched steadily higher towards the upper end of the historical range. Any attempt by Iran to increase exports would likely involve tapping onshore and floating inventories, making it important to watch for any sudden, large draws.

- The interaction between waterborne flows and inventories is vital to understanding sanctioned countries, like Venezuela and Iran, which in turn requires monitoring “dark” ships using satellite imagery (i.e. SAR).

Another important datapoint has been Caribbean crude inventories, a region that serves as a barometer for broad oil market conditions. Current storage levels are the lowest since May 2020. Read more in this Bloomberg article citing our data (terminal subscription required).

Auto Manufacturing

Auto makers have been hit hard in 2021 by the global shortage of semiconductors, an essential component for new vehicles, a topic we discussed earlier.

How long will the shortage last? How badly will auto manufacturers be hurt? Which ones will fare worse than others?

To answer these types of questions, Ursa Space monitors auto factories around the world for observable, physical activity that can signal changes in production. The list includes sites in:

- Americas: Brazil, Mexico, United States

- Asia: China, India, Japan, South Korea

- Europe: France, Germany, Italy, Russia, Spain, United Kingdom

By manufacturer, the list covers: BMW, Changan, Fiat, Ford, GM, Hyundai, Jaguar Land Rover, Kia, Nissan, PSA, Renault, SAIC-GM, Tesla, Toyota, and Volkswagen, among others.

For more information, you can watch a short video or check out this story map.

Our Auto Manufacturing Index (AMI) captures vehicle production trends that can be used to analyze car maker performance and discover macroeconomic signals.

What do recent trends show?

In light of the semiconductor chip shortage, wreaking havoc on the auto industry, it’s important to note that the Global AMI fell this month to its lowest point on record, according to our data going back to the start of 2016.

This marks a turnaround after the Global AMI recovered in late 2020, signaling at the time that the auto manufacturing sector had survived the pandemic and could steadily rebound.

To be fair, not every country could be said to have entered a state of recovery (e.g., Brazil, India), though the likes of China and the United States helped paint a relatively rosy picture for the industry as a whole heading into 2021.

After a nosedive in the first quarter of 2020, China’s AMI bounced back and remained stable for the remainder of the year. Though it began to drift lower in early 2021, it wasn’t until June that China’s AMI plunged, driving the Global AMI lower.

What do you think happens next? Have we entered a period of higher inflation? Or will supply catch up with demand once the backlogs caused by the pandemic are sorted out?

In the meantime, let us know if you’d like to learn more about this or any of our other products and capabilities.