Global crude stock builds eased before price rebound

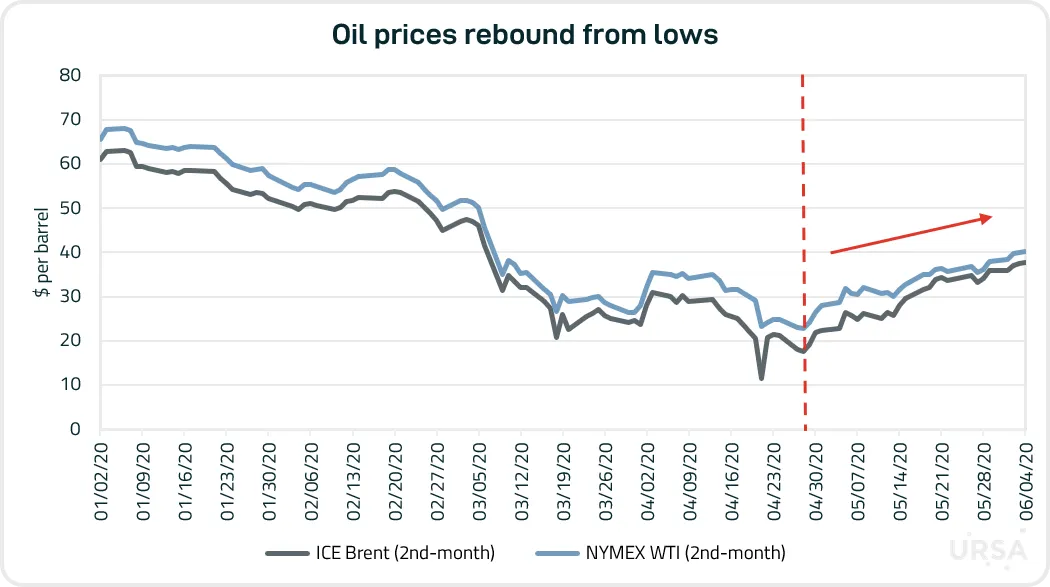

After a historic collapse, oil prices have been increasing, an impressive turnaround since being in free fall earlier this year.

A few weeks before hitting bottom, there were signs of fundamentals improving, providing a leading indicator for prices (keep reading).

Production cuts (OPEC, Russia, US shale), better-than-expected gasoline demand, and hopes for an economic recovery have helped lift oil prices.

The oversupply could shrink and even switch to a deficit later in the year, according to some analyst forecasts.

Sources: CME Group, IntercontinentalExchange

A more direct way of measuring the supply-demand balance is through inventories.

Global crude inventories increased in February and March in response to oil demand plummeting as Russia and OPEC cranked up production to fight for market share.

By April, the talk-of-the-town was storage running out in a matter of weeks, a nightmare scenario putting further pressure on oil prices.

Yet, the data painted a different picture.

This data on global crude inventories comes from Ursa. We measure floating-top tanks on a weekly basis using satellite radar imagery.

Figure 1 chronicles the following sequence of events.

Figure 1

First, the extent of builds wasn’t as severe as widely depicted.

Global crude inventories peaked just above 60% of nameplate capacity.

Granted, the actual capacity utilization is higher because tanks cannot be filled all the way for safety and operational reasons. There is also a minimum level below which suction pumps are ineffective.

Second, an inflection point occurred in early April, marking a shift in the trajectory of inventories.

Weekly builds became much smaller than during March, and there were even a scattering of weekly draws.

The biggest driver behind the curve flattening was China, which was also responsible for the steep builds in March.

Given the path of the coronavirus outbreak, it’s not surprising that China would be the first country to register large builds and subsequently lower inventories.

Europe, on the other hand, began to build inventories a few weeks after China, and continues to do so.

This difference between China and Europe can be broadened to countries outside OECD and those belonging to the organization.

Figure 2 depicts crude inventories for OECD and non-OECD countries.

Figure 2

If you want a closer look, we’ve created an interactive dashboard containing Ursa’s oil storage data.

Watch the video below to take a tour:

","url":"https://vimeo.com/426026940","width":426,"height":240,"providerName":"Vimeo","thumbnailUrl":"https://i.vimeocdn.com/video/903948574_295x166.jpg","resolvedBy":"vimeo"}" data-block-type="32">

" data-provider-name="Vimeo">

One of the aims in building our dashboard was capturing inventory levels in relative terms. How full are stocks versus what is considered “normal”?

Every week, we compare a country’s latest capacity utilization level versus that country’s mean. We then categorize each country as either:

-

High: One standard deviation above the mean

-

Mid: Within one standard deviation of the mean

-

Low: One standard deviation below the mean

Each country is displayed with a circle colored green (high), white (mid) or orange (low).

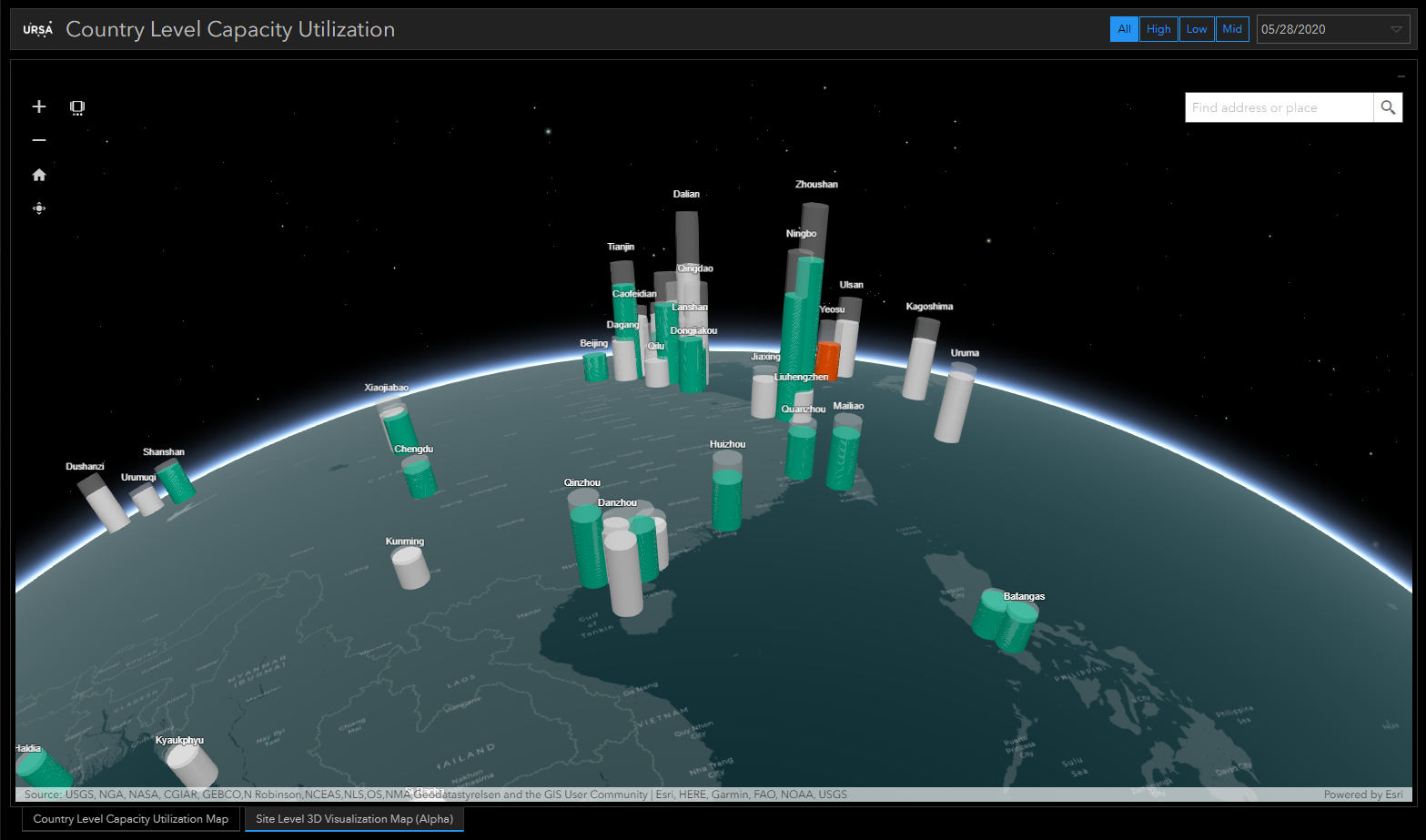

Figure 3 shows a country-level map with data from May 28th.

Figure 3

The latest breakdown is 25 countries (high), 23 countries (mid) and 8 countries (low).

This was the first week in which the “high” category ranked number one; however, considering the trends, it was just a matter of time.

You can see this data going back to March 2018 on the dashboard, shown in Figure 4:

Figure 4

The white line (number of “mid” countries) has fallen steadily in 2020, while the green line (number of “high” countries) has been ascending.

You can also check out our coverage by viewing a 3D map in the dashboard (Figure 5).

Figure 5

Each site is shown on the map. The colors - green, white, and orange - refer to the same designation.

The heights of the cylinders are proportional to the fill levels (shaded area) and capacity (transparent area).

What comes next in terms of oil inventories and prices will partly hinge on whether supply remains constrained or not.

The voluntary component is OPEC & Russia, who agreed to a record cut of 9.7 million barrels per day (bpd) in May and June.

A virtual ministerial meeting is tentatively scheduled for this month.

The involuntary component is US shale production, which has fallen in the face of low oil prices.

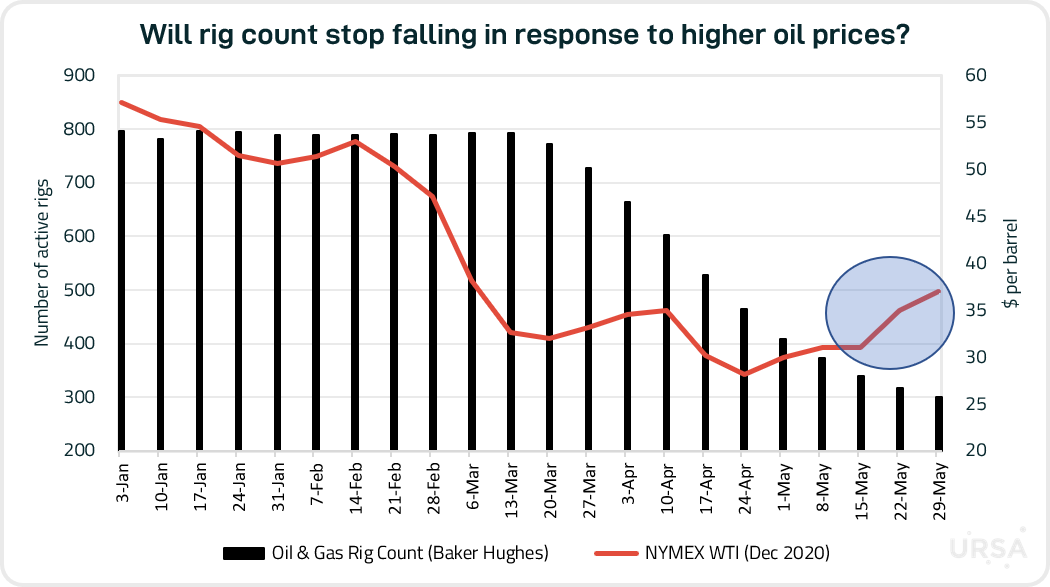

The number of active rigs has dropped to the lowest ever (Figure 6), causing a significant drop in production (Figure 7).

Figure 6

Figure 7

Typically, drilling follows oil prices, as happened during the latest downturn. Oil prices crashed in March. The rig count fell in April.

As production then declined, this gave a reason for oil prices to firm, yet the rig count hasn’t responded yet (Figure 8).

Figure 8

But how much longer will this last? Will drilling resume at current prices? Or are producers waiting for higher prices and better fundamentals?

There are already some media reports suggesting shale companies are returning, a prospect that could complicate OPEC/Russia negotiations.

An increase in US shale production would also weigh on oil prices, if demand is inadequate to absorb the additional supply.

We will continue to monitor these developments and provide updates.

You can also visit our COVID-19 Dashboard for continuous updates on the local, regional and global impacts of the pandemic.