An economic scorecard: China, Europe, US

Data derived from satellite imagery can offer fresh clues about the relative economic conditions in China, Europe and the US. The standings of these economies have emerged as a key issue in 2020, driven by the winding global path of the coronavirus outbreak.

This data can provide a near real-time, ground-truth signal regarding the economic impact of a second wave of coronavirus, as well.

A surge in coronavirus cases in the US and Europe has greatly diminished expectations for economic growth. Meanwhile, in China, the story has been one of a V-shaped recovery, though plenty of doubts exist as to whether reality is as rosy as official data suggests.

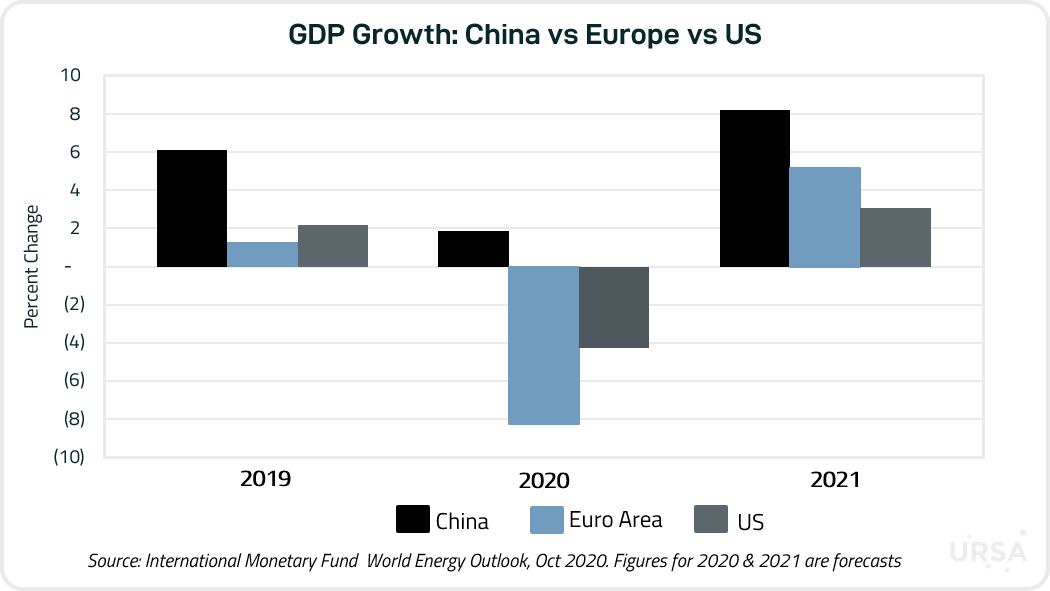

The disparities are apparent in the latest GDP forecasts by the International Monetary Fund (IMF). The Euro Area (-8.2%) and the US (-4.2%) will likely contract in 2020, while China (+1.8%) will eke out a modest gain, according to the IMF.

For more insight, let’s turn to two global datasets provided by Ursa Space: crude oil inventories and auto manufacturing activity.

Both datasets are derived from data collected by the company’s Virtual Constellation of synthetic aperture radar (SAR) satellites, which offer unique all-weather, day/night detection capabilities.

Our global coverage includes roughly 200 oil storage locations and dozens of large auto plants, including those in the US, China and Europe.

The auto manufacturing index captures how many finished vehicles are stored in lots adjacent to factories, which can indicate production trends.

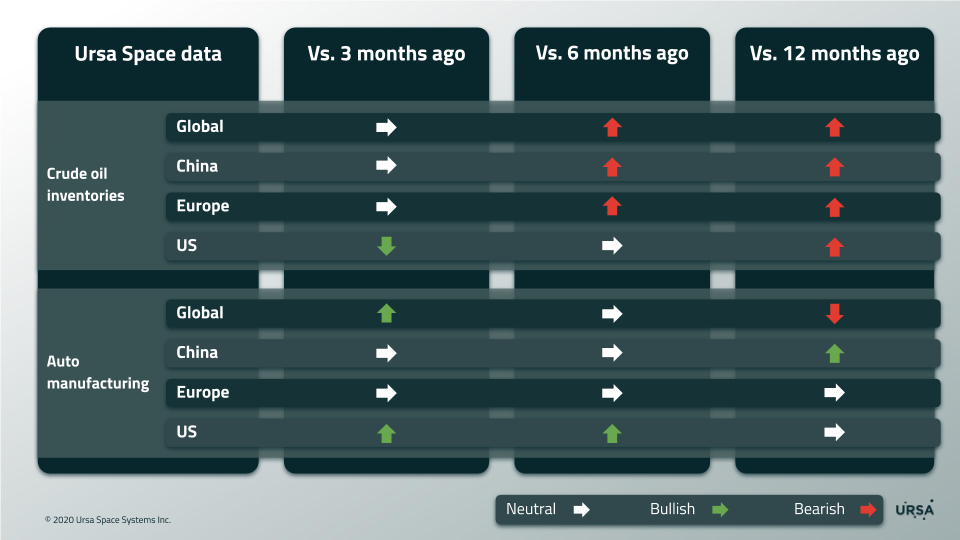

The scorecard below provides a snapshot of these indicators organized by country/region (Global, China, Europe, US).

The direction of the arrow indicates whether crude oil inventories or the auto manufacturing index are roughly higher, lower or equal today versus 3, 6 and 12 months ago. The color of the arrow represents the market implication being either bullish (green), bearish (red) or neutral (white).

Why did we choose these indicators?

Crude oil inventories represent the supply-demand balance in the oil market, which can be a sign of the economy’s status.

The automotive industry is critical, both as a large source of employment and as an economic bellwether. Coronavirus has been a challenge from the perspective of creating a safe working environment. It has also elevated uncertainty with regard to volume of auto sales.

Here are 10 takeaways, relating to both types of datasets:

- China’s crude oil inventories have fallen since September after an unprecedented period of builds from March through August. Inventory builds from March to April were caused by weak energy demand as refiners slashed runs.

- The principal reason for China’s inventory builds since May was record-setting imports, as the country went on a buying spree, snapping up cheap cargoes after oil prices fell.

- With China dialing back imports, a major source of demand has been removed from the global oil market, putting downward pressure on prices.

- China might not resume aggressive buying until inventories return to more normal levels. As of end-October, China’s 2020 crude oil inventories were 19% and 25% higher than those of 2019 and 2018, respectively.

- Over the medium-term, China’s crude appetite won’t be waning. More refineries are coming online, which means more demand. China will allow private refiners to import 20% more oil in 2021 versus 2020.

- US and European crude inventories have edged lower of late; however, both will face upward pressure if refinery demand slows on account of rising coronavirus cases. A rebound in US oil production could push its inventories even higher.

- China’s auto manufacturing activity fell sharply from February until mid-March, followed by a strong rebound that continued through June, part of the country’s supposed V-shaped recovery.

- In July, China’s auto auto manufacturing activity index dipped, but since then, it has settled into a stable range well above the mid-March low and even higher year-on-year.

- The US auto manufacturing index has increased steadily since late July, returning to levels seen before the coronavirus. This rebound pared the losses from March-July when the US auto manufacturing index plunged, reflecting a wave of plant shutdowns.

- In Europe, pockets of strength during the first coronavirus wave helped stabilize the auto index, preventing a noticeable decline. The ongoing spike, however, is more widespread and therefore represents a bigger risk to the industry.

Check back here for more updates on how satellite imagery can reveal insights about the state of the global economy.

If you’re interested, sign up for a free evaluation of our data.